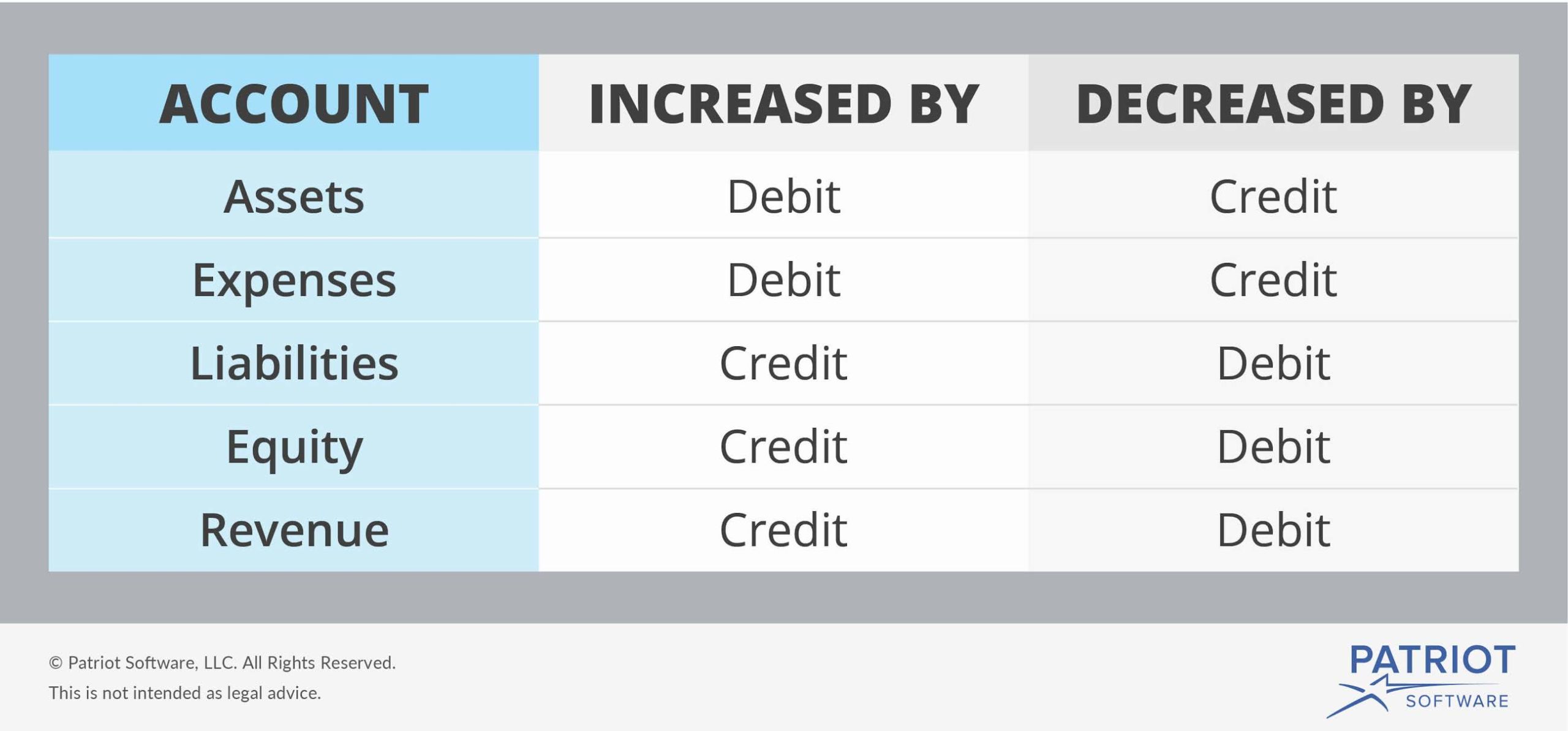

Debit Drawing Credit Capital. the accounting equation can be expanded to incorporate the impact of drawings and profit (ie income less expenses): the accounting transaction typically found in a drawing account is a credit to the cash account and a debit to. a debit balance in drawing account is closed by transferring it to the capital account. the typical accounting entry for the drawing account is a debit to the drawing account and a credit to the cash account (or whatever asset is being withdrawn). capital is recorded on the credit side of an account. likewise, the journal entry to clear the drawings account at the end of the accounting period will be the debit of. Any increase is also recorded on the credit side. It does not directly affect the profit and loss. a journal entry closing the drawing account of a sole proprietorship includes a debit to the owner’s capital account and a credit to.

from www.patriotsoftware.com

the typical accounting entry for the drawing account is a debit to the drawing account and a credit to the cash account (or whatever asset is being withdrawn). It does not directly affect the profit and loss. capital is recorded on the credit side of an account. the accounting equation can be expanded to incorporate the impact of drawings and profit (ie income less expenses): the accounting transaction typically found in a drawing account is a credit to the cash account and a debit to. Any increase is also recorded on the credit side. a debit balance in drawing account is closed by transferring it to the capital account. likewise, the journal entry to clear the drawings account at the end of the accounting period will be the debit of. a journal entry closing the drawing account of a sole proprietorship includes a debit to the owner’s capital account and a credit to.

Accounting Basics Debits and Credits

Debit Drawing Credit Capital likewise, the journal entry to clear the drawings account at the end of the accounting period will be the debit of. the typical accounting entry for the drawing account is a debit to the drawing account and a credit to the cash account (or whatever asset is being withdrawn). likewise, the journal entry to clear the drawings account at the end of the accounting period will be the debit of. the accounting transaction typically found in a drawing account is a credit to the cash account and a debit to. It does not directly affect the profit and loss. the accounting equation can be expanded to incorporate the impact of drawings and profit (ie income less expenses): a debit balance in drawing account is closed by transferring it to the capital account. capital is recorded on the credit side of an account. Any increase is also recorded on the credit side. a journal entry closing the drawing account of a sole proprietorship includes a debit to the owner’s capital account and a credit to.